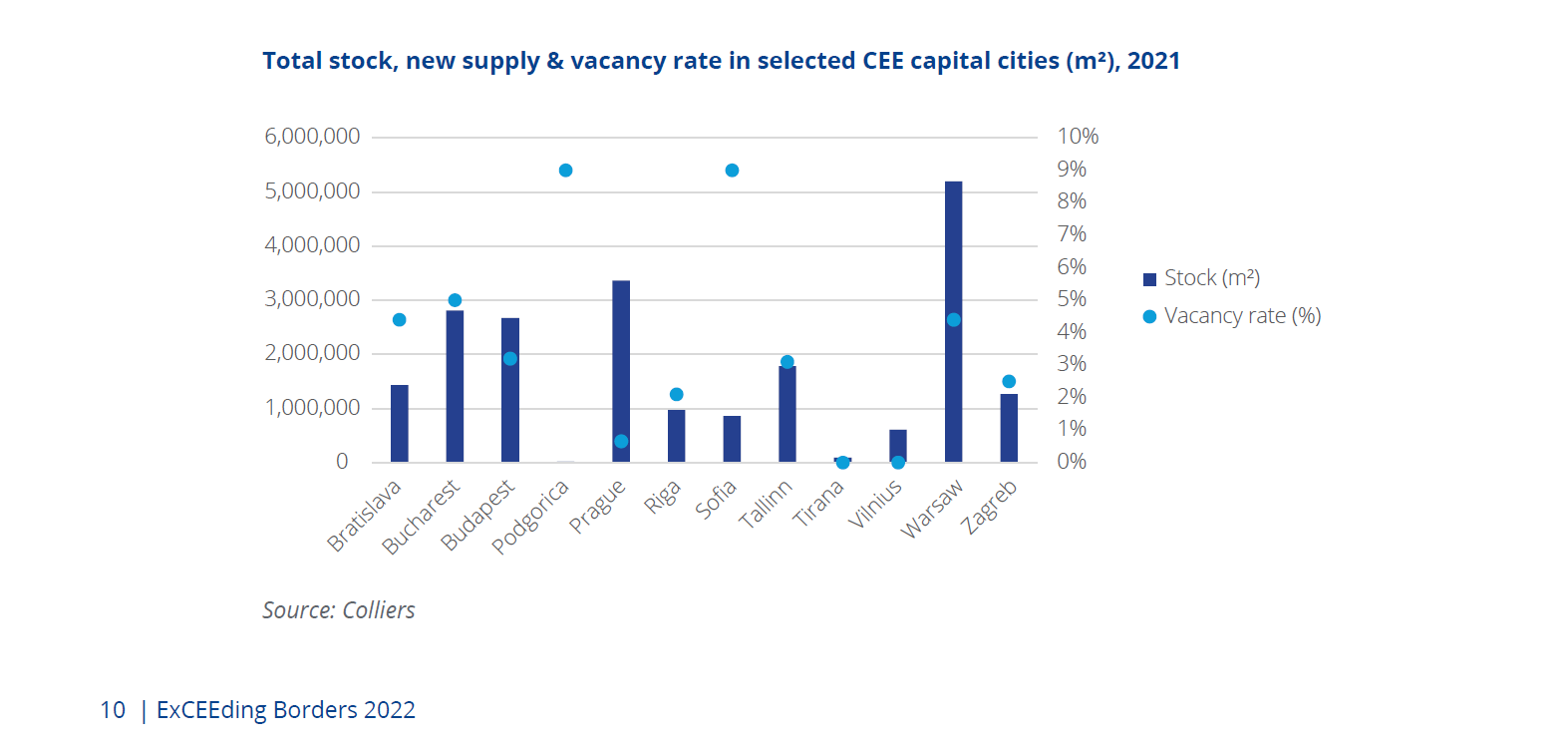

The Industrial & Logistics property sector has continued to thrive and the total I&L stock for the CEE-15 region has grown within last two years to exceed 50 million m², with 20 million m² situated in and around the 15 capital city markets. Poland, as the largest country of the group covered in the most recent ExCEEding Borders Colliers report, also maintains the largest I&L market and is approaching the 25 million m² mark.

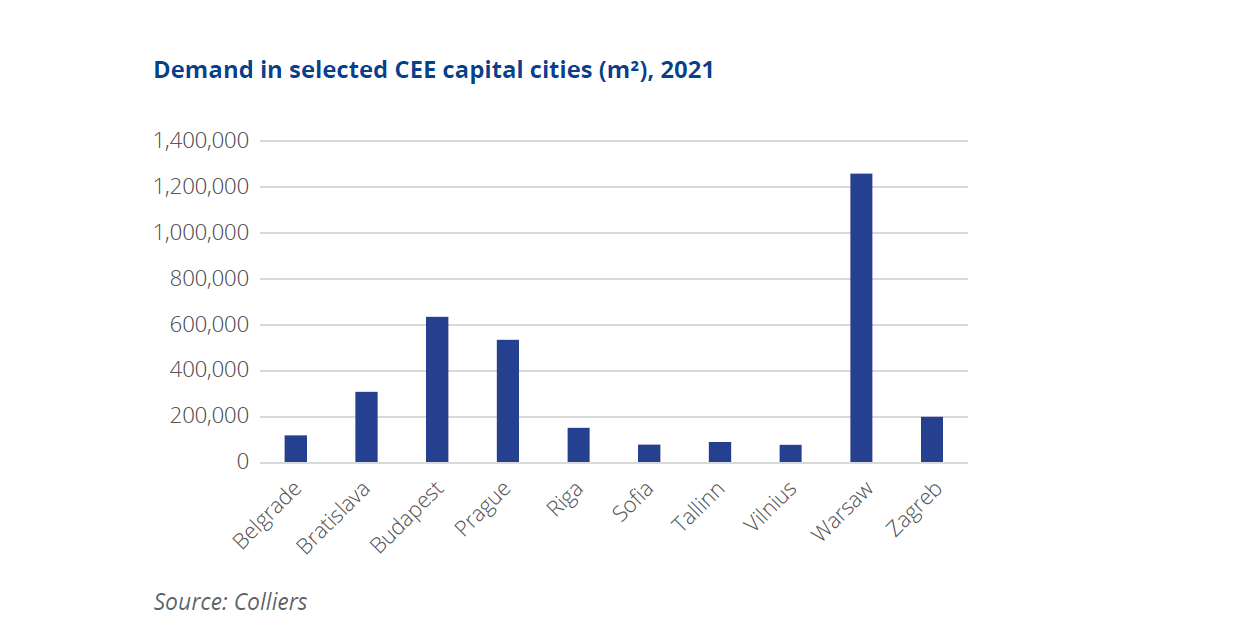

Overall, the demand from the I&L sector in the CEE-15 region over the past few years has been strong and driven mainly by the 3PL, retail and distribution sectors, followed by the light production, automotive and FMCG industries. During the pandemic, Colliers teams experienced higher tenant interest from the e-commerce sector and logistics operators offering their services to retailers and Internet trading companies. The trend toward e-commerce will continue to grow, but this growth will be slower than at the beginning of the pandemic, according to the report.

SBU / Last Mile Logistics Sector in CEE-15

Something that is often debated is the definition of what small business units (SBUs) and last mile logistics (LML) are. Therefore, we outline our guidelines on this, as we see them relating to the CEE region: SBUs are warehouses located on or near the outskirts of cities or business centres. They have convenient access to public transport, roads (expressways, motorways) or railways, which ensure fast delivery. These schemes, as opposed to standard big box warehouses, can comprise both warehouse and office space as well as showrooms or retail premises. SBUs – as the name suggests – are made up of small business modules, which offer high flexibility. The average size of a single module is usually 500 m². It is possible to combine modules and adapt space to the needs of tenants if companies need to rent more space than a standard module. Since the size of SBU warehouses are not large, they are suited to small and medium-sized companies.

LML units are also small city warehouses made up of small modules with high flexibility. However, they are slightly larger than SBUs, with a standard module being 1,500 – 3,000 m². They are city warehouses and they used to be located around larger cities. Last mile projects are most often leased by tenants from the e-commerce and courier sectors.

The total stock of typical SBU / Last Mile Logistics space in the CEE-15 countries accounts for over 3 million m². The development of this market is not evenly spread among the CEE-15 countries. In fact, each of them is at a different stage of development. There are some countries where there are no typical SBU/LML schemes at all, such as Albania or Bosnia and Herzegovina. In that case, specific tenants in this sector lease smaller modules in big-box or smaller I&L schemes of lower standards. Some projects are also built with a concept similar to modern SBU/LML schemes, but for private use. The largest amount of space is located in Poland (ca. 2 million m²). The country with the biggest share of SBU/LML space of its total I&L stock is Bulgaria, where this type of schemes account for 59% of total supply. Other countries with noteworthy shares are Estonia (13%), Hungary (13%) and Poland (8%).

In CEE-15 there is ca. 500,000 m² of SBU/LML space under construction. The majority of that volume is being built in Poland (310,000 m²). Other countries with a significant volume of space under development in CEE-15 are Estonia (68,000 m²) and Bulgaria (54,400 m²), according to the Colliers report.

Typically, rents and service charges are significantly higher than in standard buildings, but SBU and LML spaces make up for this with excellent locations and excellent adaptation to needs. All of these factors result in higher construction costs. In most of the CEE-15 countries headline rental rates for this type of space range between EUR 3.5 – 7.0 per m²/month but, in the Czech Republic and Estonia, they can even reach the level of EUR 12 per m²/month (mainly in SBU schemes).

In summary, all CEE-15 countries have seen an increase in enquiries for SBU/LML space. This is connected, among others, with the significant development of the e-commerce sector and courier services. These factors mean that in the coming quarters we can expect further significant development of this market segment in CEE-15.

„The total stock of typical SBU / Last Mile Logistics space in the CEE-15 countries accounts for over 3 million m². The development of this market is not evenly spread among the CEE-15 countries. In fact, each of them is at a different stage of development”, Antoni Szwech Analyst, Research and Consultancy Services | Poland, Colliers